Hebdo Crédit Octo 05/22/2026 “The change of regime does not put Credit on a diet” By Mathieu Cron, Amplegest

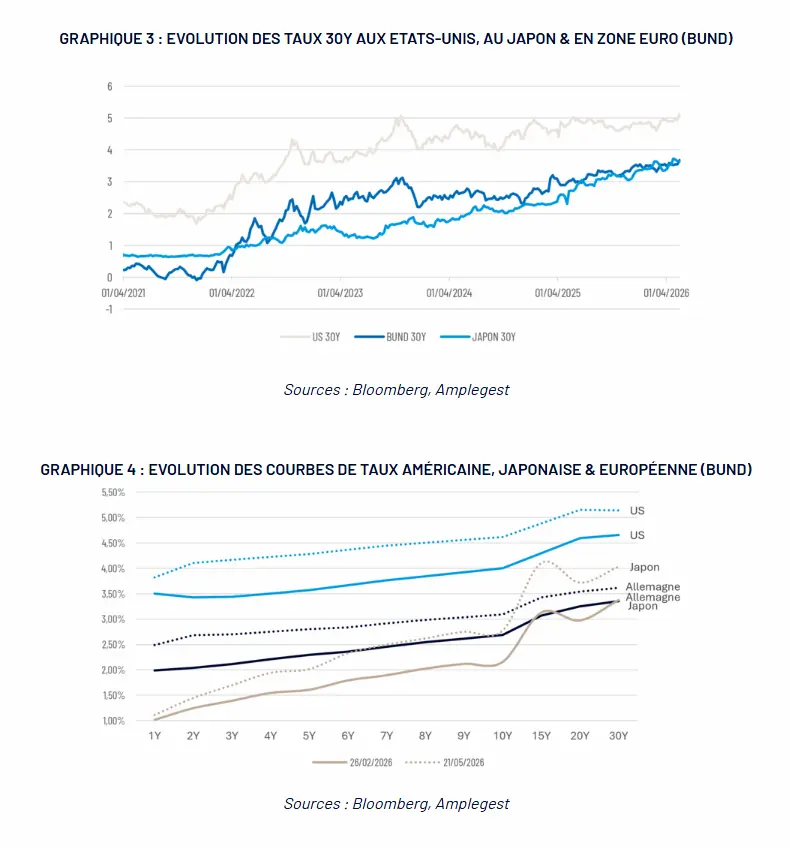

From TACO (“Trump always Chickens Out†– Trump always ends up running away) to NACHO (“Not a Chance Hormuz Opens“, No chance that the Strait of Hormuz will be reopened). From a behavioral bias making it possible to anchor the resilience of markets to the most acute geopolitical crises, to an awareness of the risks induced by a (late) prolongation of the Iranian conflict, through statistical publications likely to invalidate the accommodating rate scenario which has long maintained the indolence of investors. Or how, according to the interest rate markets (see graphs below), investors seem to have integrated, as surely as late, a triple reality: that of the extent of the supply shock on fossil raw materials induced by the strangulation of the Strait of Hormuz (1) and the risks which it carries, not only in terms of global inflationary pressure (2), but also in terms of acceleration of the process of asserting “fiscal dominance” to the detriment of monetary credibility (3).

Read also: Iranian crisis: should we review our investment optimism?

See also: Market volatility: should we be defensive or opportunistic?

.webp "Do markets still underestimate geopolitical and inflationary risks?")

â€

An oil shock that could sustainably fuel inflation

Without denying the importance of this change in “regime”, it seems essential to us to go beyond the excessively noisy comments which have too often accompanied it in recent weeks to try to appreciate its real significance. Are we really justified in believing that investors and their artificial proxies have fundamentally changed their understanding of the risk environment in which it is up to us to invest? Are we really justified in thinking that investors have finally chosen to address the massive dissonance that has prevailed for many months between the level of global uncertainty (economic, political and geopolitical) and market valuations?

You will certainly have anticipated it: there is every reason to believe that not, and to lean towards a relaxation on rates at the moment when a solution to the Iranian conflict and the beginning of the beginning of a reopening of the Strait of Hormuz materializes, the investors who have clearly largely chosen to consider:

- that the price of oil is, more than a proxy for inflation, THE explanatory variable of its evolution

- therefore, that even a very gradual normalization of traffic in the Strait of Hormuz will be enough to extinguish the risks of a global inflationary slide.

Read also: Oil: the barrel drops below 100 dollars thanks to hopes of an agreement with Iran

Hay warnings from the International Energy Agency (see Interview with Fatih Birol on France Inter of April 21, 2026 and Oil Report of May 13, 2026) on the unprecedented scale of the supply shock caused by the Iranian conflict and the fact that, even assuming a rapid loosening of the grip of Hormuz, taking into account the deterioration of global stocks of petroleum products, it is illusory to believe in a return to normality of energy prices before 2 years. Gone are the lessons offered by the Ukrainian crisis on the reality of the mechanisms for the diffusion of an inflationary shock throughout all the links in the supply chains and the distortions that this diffusion is likely to have on: 1. company margins and 2. consumer behavior (see graph below).

Read also: The Strait of Hormuz and the markets: when oil redefines monetary policy

â€

.webp)

Credit spreads returned to pre-crisis levels

And if these elements were not enough to convince you of the persistence of a major dissonance between global macroeconomic, political and geopolitical reality and the valuation of the markets, despite the correction of the interest rate markets, undoubtedly the evolution of credit spreads over the period recent research will allow us to establish our argument more definitively.

As the graphs below show, credit spreads (in other words, credit risk premiums) have returned to levels comparable to those which prevailed before the outbreak of the Iranian conflict, to the point of offering no reflection of the risks that surges in inflation and anticipated rate increases are likely to pose to their balances. by investors.

While it is quite obvious that these valuations are linked to the renewed attractiveness of credit in a context of growing distrust towards sovereigns and their immediate and medium-term prospects (to mention only the markets related to our investment universe) – in other words with technical elements particularly powerful, they nonetheless raise questions.

Read also: A new index of tension on rates to watch

Artificial intelligence and monetary tightening: two opposing scenarios

If a conflict long considered impossible because its negative potential is unpredictable has not resulted in a lasting correction of credit premiums, we can in fact only be justified in questioning the nature of the elements likely to reduce the major cognitive dissonance of which they are the witness. At this stage we see two – one marked by frenzied optimism, built around a narrative of a jump in productivity induced by the large-scale adoption of artificial intelligence; the other, more immediately pessimistic, of tightening credit conditions.

To use an optimistic argument dear to the new President of the FED (among others), the jump in productivity to be expected from advances in (the adoption of) artificial intelligence is such that it is likely to erase all inflationary pressures, whatever their origin. In particular, as the process of diffusion of the oil supply shock in the various global supply chains is far from immediate, it is all the more likely to be offset by productivity gains achieved before its full materialization in prices. This pleasant narrative nonetheless suffers from obvious weaknesses: it forgets that the conditions necessary for the large-scale adoption of different artificial intelligence tools are far from being met (see the contributions of Sam Altman, Dario Amodei and Arthur Mensch on this subject), just as much as it ignores the consequences that these advances are likely to have in terms of income distortion (between socio-professional categories) and consumption.

Conversely, the argument relating to a possible credit crunch refers to a plurality of potentially converging elements: an increase in European key rates from next June 11, as anticipated by a market which nevertheless pretends to ignore the potential of such a movement in terms of deterioration of an already fragile economic phase; a materialization of the desire hammered out by the dove Warsh throughout its journey to the pinnacle of the FED, to see the balance sheet of the institution decline; a more global tightening of monetary policies across the globe in response to the oil shock. A plurality of elements which cannot have any other translation than a reduction in this very liquidity which supports, despite and against any other fundamental consideration, most of the current valuations of financial assets.

Read also: AI and markets: business confidence at its highest since Covid

A cautious strategy in the face of market uncertainty

Faced with such realities, we have for the moment chosen to maintain our cautious positioning and continue to plow the Value furrow that constitutes us in the hope of overcompensating for the negative impact of this prudence on the relative performance of our funds, rather than fundamentally becoming risk buyers again. To take the elements of a recent exchange with a Parisian institutional player, for things to be otherwise, two conditions would have to be met: 1. That the credit risk premium levels on High Yield have reached – at least – their historical average; 2. May the thick fog in which we are collectively forced to operate dissipate a little.

By Mathieu Cron, Amplegest

/2026/06/11/6a2a4ee24803c565853794.jpg "REPORTING. “On the front, the sky is literally teeming with drones”: how the Ukrainian army trains to face the threat")