The IFPEN meeting for a weekly analysis of the situation on the oil markets.

Â

May 18, 2026

Brent starts to rise again after a Trump summit – Xi Jinping without progress on the conflict in the Middle East

Crude oil prices ended the week higher, with Brent on the futures markets closing the week near $110/bbl.Market operators had high expectations of the meeting between American President Donald Trump and his Chinese counterpart Xi Jinping, hoping that Beijing, in its capacity as the leading buyer of Iranian crude, would exert decisive pressure on Tehran to restore free movement across the strait of Hormuz. Even if China has declared that the Strait of Hormuz must be reopened as quickly as possible, its lack of active involvement in the management of this conflict does not suggest a rapid resolution of the conflict and raises fears that the United States and Israel will tighten their pressure measures against Iran, or even consider a resumption of military operations.

Following Iran’s announcement that it had authorized the passage of around 30 ships, traffic in the Strait of Hormuz increased slightly last week, which somewhat improved market sentiment. However, the situation in the strait remains tense. This weekend, the Iranian government announced the establishment of a royalty system, presented under the guise of maritime insurance policies, while continuing its strategy of pressure and inducement towards ships operating in the Persian Gulf. This approach is part of a broader desire to normalize and consolidate Iranian control over the strait. This mechanism appears to have been designed to be politically and commercially more acceptable than an explicit toll, since it is presented as “maritime insurance”, but should be rejected by the international community.

![]() Â Read more / Download the dashboard (PDF -Â 430 Ko)

Read more / Download the dashboard (PDF - 430 Ko)

Â

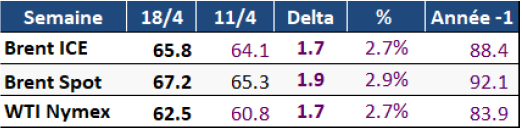

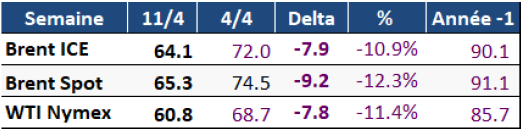

May 11, 2026

Despite an increase in attacks, the hope of a diplomatic solution to the conflict in the Middle East brings down the price of oil

Crude oil prices fell last week, supported by hopes of a diplomatic outcome to the conflict in the Middle East, despite an upsurge in violence reaching levels not seen since the announcement of the ceasefire last month.Â

Tensions in this region have indeed greatly intensified last week. Iran again targeted the oil industrial zone of Fujairah in the United Arab Emirates, as well as Kuwait, and launched fast boats against American destroyers in the Strait of Hormuz. Tehran also announced the seizure of an oil tanker. In response, the United States carried out strikes against several Iranian military sites and neutralized two Iranian oil tankers attempting to breach the blockade.

Despite this resumption of hostilities, several press sources indicate that negotiations between Washington and Tehran are continuing around a temporary framework agreement aimed, initially, at allowing the reopening of the Strait of Hormuz. This perspective helped to alleviate fears of an immediate escalation explaining the decline in oil prices.

On Sunday, the official Iranian news agency IRNA indicated that it had transmitted its response to the latest American proposal, without however giving further details. The American president described the Iranian response as unacceptable. In this context, crude prices started to rise again this morning, to nearly $104/bbl. Markets are now paying attention to the meeting planned for this week between the American and Chinese presidents, which could increase pressure on Iran to reach an agreement.

![]() Â Read more / Download the dashboard (PDF -Â 430 Ko)

Read more / Download the dashboard (PDF - 430 Ko)

Â

May 4, 2026

The diplomatic standoff between the United States and Iran, combined with continued disruptions in the Strait of Hormuz, continues to support oil prices. Brent at more than $110/bbl.

Brent reached a weekly peak of $126.4/bbl last week, its highest level since March 2022, before falling back to close at $108/bbl. This correction movement seems mainly technical rather than fundamental. Analysts explain this in particular by profit taking, effects linked to the expiration of contracts, as well as by large volumes of sell orders.

Geopolitically, negotiations between the United States and Iran are stalled due to major differences over Iran’s nuclear program, sanctions regime and control of the Strait of Hormuz. The latest Iranian proposals, transmitted to the American authorities this weekend, would provide for the establishment of a one-month deadline to reach an agreement aimed at reopening the Strait of Hormuz, lifting the American naval blockade and putting an end to hostilities in Iran and Lebanon. If an agreement is reached, a new round of one-month negotiations could be initiated to deal with the question of the nuclear program. In response, US President Donald Trump indicated that he would examine this proposal, while expressing reservations about its feasibility and not closing the door to a resumption of military strikes.

In this context, the fundamentals of the oil market continue to tighten as the conflict continues.

Seasonal demand contributes to accentuating these tensions: the increase in fuel consumption during the summer, combined with limited supply, should support prices. The marked drop in inventories of crude oil and petroleum products in the United States last week confirms this feeling of tightening supply, combined with increasing demand as summer approaches.

![]() Â Read more / Download the dashboard (PDF -Â 430 Ko)

Read more / Download the dashboard (PDF - 430 Ko)

Â

27 avril 2026

Ninth week of war in Iran. Brent returns above $100/bbl with the impasse in peace talks.

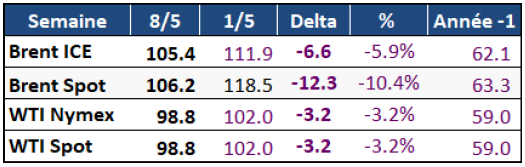

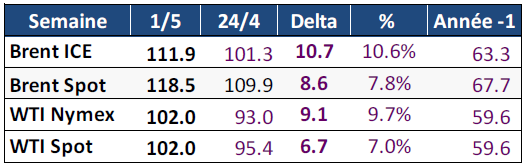

Last week, crude oil prices started to rise again, driven by an intensification of tensions in the Middle East and the stagnation of peace talks. If the ceasefire is still in force, the geopolitical risk remains particularly high in the Strait of Hormuz where the United States and Iran continue to impose strong restrictions on navigation. Recent events, such as ship seizures, exchanges of threats and the maintenance of a significant naval military presence, now make safe movement in the region impossible. At the end of the week, however, the pressure eased slightly, with indications suggesting that Iran could submit a proposal intended to meet American demands, thus reviving hopes of a de-escalation. Tehran would thus have proposed an agreement aimed at reopening the strait and putting an end to the conflict, by postponing discussions on nuclear power to a later phase. Furthermore, Donald Trump is due to meet his main advisers on national security and foreign policy on Monday to examine the current situation and the impasse in negotiations.

Over the week, the average spot price of Brent fell by 6.7%, settling at $109.9/bbl, while that of WTI increased by 3.6% to reach $95.4/bbl. On the futures markets, Brent for delivery in July, on the other hand, increased by 5.7%, to $101.3/bbl. The Bloomberg consensus of April 24 was revised upwards. The expected average price of Brent now stands at $89/bbl for the second quarter (+$3.6/bbl) and $75.4/bbl for the third quarter. The most bullish consensus scenario remains unchanged, with Brent at $125/bbl in the second quarter, then $135/bbl in the third quarter (+$35/bbl) (fig. 1 and 2).

![]() Â Read more / Download the dashboard (PDF -Â 429 Ko)

Read more / Download the dashboard (PDF - 429 Ko)

Â

20 avril 2026

A geopolitical situation that is always particularly unstable and unpredictable. Brent down to $118/bbl

Last week, the oil market was in a phase of fragile stabilization, with on one side signs of gradual improvement in supply and, on the other, geopolitical tensions still very present. Following the announcement on Friday by Iranian Foreign Minister Abbas Araghchi that commercial ships were once again allowed to transit the Strait of Hormuz during the remaining duration of the ceasefire, Brent prices fell by around 15% on the spot market, falling back below the $100/bbl mark for the first time since mid-March. This announcement was, however, contradicted the next day, with declarations once again indicating a closure and strict control of the strait, which ultimately remains subject to a double Iranian and American blockade. According to shipping analysis firm AXS Marine, there are currently between 108 and 116 MB of crude oil stored on ships at sea in the Persian Gulf.

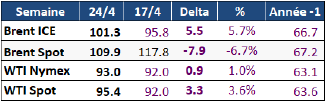

The events of recent days illustrate the unstable and unpredictable nature of the conflict, despite the diplomatic efforts deployed to contain its escalation. Donald Trump’s statements proved contradictory in the space of a few hours, while Israel continues its operations in Lebanon and Iran alternates between opening and closing the Strait of Hormuz, having even opened fire on two ships trying to cross it. While the ceasefire between the United States and Iran is due to end next Tuesday, new talks are planned for the same evening in Islamabad, in a context of uncertainty as to the evolution of the situation. This morning, on the futures markets, Brent was up 6% to more than $95/bbl.

Over the week, the average spot price of Brent fell by 10.5% to $117.8/bbl, while that of WTI fell by 10.5% to $92/bbl. On the futures markets, Brent for delivery in June fell by 5.2%, to reach $95.8/bbl. The Bloomberg consensus of April 17 forecasts an average Brent price of $85.4/bbl for the second quarter (+$7.9/bbl) and $75/bbl for the third quarter. In its most bullish scenario, the consensus now anticipates Brent at $125/bbl in the second quarter, then at $135/bbl (+$35/bbl) in the third quarter (fig. 1&2). This tends to show that a growing number of institutions are now developing long-term crisis scenarios, such as the International Energy Agency (IEA), which is studying in its latest report a protracted scenario (“Protracted Case”) in which disruptions to production in the Middle East remain high and energy flows to international markets remain severely restricted. This situation would lead to a supply deficit forcing a draw on global stocks of around 6 Mb/d, a level deemed “unsustainable”, corresponding to a cumulative loss of close to 2 billion barrels by the end of the year.

![]() Â Read more / Download the dashboard (PDF -Â 426 Ko)

Read more / Download the dashboard (PDF - 426 Ko)

Â

13 avril 2026

American blockade of the Strait of Hormuz: the hope of a rapid de-escalation with Iran is crumbling. Brent at $132/bbl

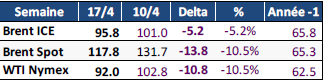

The announcement last Tuesday of a two-week ceasefire between the United States and Iran, accompanied by a conditional reopening of the Strait of Hormuz and the holding of talks in Pakistan over the weekend, led to a clear decline in the oil markets. Brent prices on the spot market fell by 14%, while those of diesel in Europe fell by 16% at the same time. The financial markets also welcomed this apparent relaxation: the S&P 500 rose by 3% and the Euro Stoxx 600 by almost 4%. This movement reflects above all a significant drop in geopolitical risk premiums, which had reached excessive levels, while investors had, in the preceding days, integrated an extreme scenario combining the massive destruction of Iranian infrastructure and a prolonged blockage of the Strait of Hormuz. HAS

Despite this apparent de-escalation, caution remained among operators, and very few ships actually transited the strait. The differences between Washington and Tehran remained deep on all the points under discussion: the Iranian nuclear program, the lifting of sanctions, the conclusion of a non-aggression pact, reparations linked to the conflict, but also the recognition of Iran’s right to enrich uranium and to fully exercise its sovereignty over the Strait. So many subjects which suggested particularly difficult negotiations. In this context, the failure of the discussions announced on Sunday hardly surprised observers. It was immediately followed by Donald Trump’s announcement of an imminent naval blockade of the Strait, following the impasse in talks on the nuclear issue.

If the precise terms of this blockade still remain unclear, it could be inspired by the system implemented against Venezuela, with an interception strategy on the high seas thus limiting the direct exposure of American forces. But beyond just Iranian ships, this measure would in practice risk paralyzing all maritime traffic in the area. Indeed, the American authorities have mentioned a control of any ship entering or leaving Iranian ports. In this context, it appears unlikely that Tehran would passively accept such a restriction. Iran could seek to retaliate by disrupting maritime traffic more widely, making navigation risky for all ships, whatever their origin. strait in an open confrontation zone, with a massive dissuasive effect on shipowners and insurers. A measure of this nature would hit Iran hard, whose oil exports via this route remain at around 2 Mb/d, but also the countries dependent on this oil, notably China and India. is moving away, leaving room for a risk of regional escalation and a new surge in oil prices This morning Brent on future markets had already gained 8% to nearly $102/bbl.

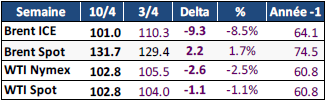

Over the week, the average spot price of Brent stood at $131.7/bbl, up 1.7%, while WTI fell 1.1% to $102.8/bbl. On the futures markets, Brent for delivery in June fell by 8.5%, reaching $101/bbl. The Bloomberg consensus of April 10 is stable with an average Brent price for 2Q, at $77.5/bbl and for 3Q, at $75/bbl. In its highest scenario, the consensus now anticipates Brent at $125/bbl in the second quarter and $100/bbl in the third quarter.

The unprecedented gap of around $30/bbl between the spot price of Brent and the future price constitutes an unprecedented phenomenon in the history of oil markets. It reflects both extreme tension on the physical market, marked by an immediate scarcity of crude, the confidence of financial markets in medium-term normalization, and a persistent disorganization of logistical flows. In this context, Bloomberg reported last week that, on the physical Brent market, 40 purchase orders had only resulted in four transactions actually concluded. According to operators, these panic movements in the main physical places reflect the extent of the anticipated gross deficit as the conflict continues.

![]() Â Read more / Download the dashboard (PDF -Â 430 Ko)

Read more / Download the dashboard (PDF - 430 Ko)

Â

7 avril 2026

Brent is approaching $130/bbl in a context of complete blockage of the situation in the Middle East

In March, Brent saw one of the biggest monthly gains in history, jumping about 64% to $127/bbl.while the Strait of Hormuz, a crucial transit route for nearly 20% of the world’s oil supply, remained virtually closed by the Iranian authorities.

This situation maintains extreme volatility on the futures markets, which react brutally to each declaration from the warring parties. Last Tuesday, rumors of de-escalation, suggesting a possible openness of Tehran to a conditional ceasefire, caused a sharp correction of Brent on the futures markets, accentuated by the expiration of the May contract. But this respite was short-lived: from Thursday, prices resumed their rise, with WTI jumping by more than $11/bbl in a single day, its strongest absolute increase since 2020 following signals announcing an intensification of American military operations against Iran. Notably, WTI briefly exceeded Brent during this session, a rare reversal reflecting the extreme tension on US physical supply in the short term. The closure of the financial markets for the Easter holidays interrupted the rise in quotations, but on Monday, on the Nymex, WTI was again quoted at more than $112/bbl, while the American president reiterated his ultimatum towards Iran.

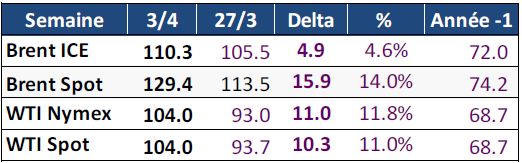

Over the week, the average spot price of Brent stood at $129.4/bbl, up 14%, while WTI rose 11%, to $104/bbl. On the futures markets, Brent for June delivery rose 4.6% to $110.3/bbl, and WTI rose 11% to $104/bbl. The Bloomberg consensus of April 6 revised upwards its average Brent price forecasts for 2Q, to $77.5/b (+$2.9/b), and for 3Q, to $75/b (+$3.5/b). In its highest scenario, the consensus now anticipates Brent at $125/b in the second quarter (+$15/b) and at $100/b in the third quarter (+$5/b).

Calendar spreads continue to soar, reaching new all-time highs. Spreads on the closest futures contracts on major oil markets, usually expressed in cents, have now exceeded $10/bbl. The gap is even more marked for WTI, which crosses $14/bbl, thus approaching its highest level ever recorded. This strong differential between the two closest contracts reflects expectations of a tightening of supply in the United States, as foreign buyers turn to American oil to compensate for Middle Eastern crude.

![]() Â Read more / Download the dashboard (PDF -Â 490 Ko)

Read more / Download the dashboard (PDF - 490 Ko)

Â

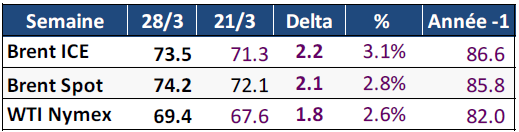

30 mars 2026

After a month of fighting, skepticism remains about the likelihood of a short-term ceasefire. Brent rises to $113/bbl

At the start of last week, oil prices fell by around 11% after the United States announced a five-day postponement of its ultimatum for military strikes against Iranian energy infrastructure, while ongoing diplomatic discussions were considered constructive for defuse the conflict. However, in the absence of significant progress between the two parties, the continuation of mutual bombings, the arrival of new American troops and especially the maintenance of the quasi-blockade of the Strait of Hormuz caused prices to rise again, closing the week at around $113/bbl.

Prices were also supported by Ukrainian attacks on Russian energy infrastructure. The port of Ust-Luga, on the Baltic Sea, was again damaged by a Ukrainian drone strike, in a context of intensified operations targeting Russian oil installations. Loading operations have been paralyzed there for several days; another strategic site, the port of Primorsk, was also affected. These two terminals alone provide almost half of Russia’s maritime crude oil exports.

At the same time, the attack launched this weekend by the Houthis against Israel is rekindling tensions in the Red Sea. Supported by Iran, the latter fired ballistic missiles in retaliation for American-Israeli strikes against Iranian nuclear installations. Their activity could weaken the situation around the port of Yanbu, through which Saudi Arabia sells up to 7 Mb/d and the only real bypass of the Strait of Hormuz currently available. For now, the Houthis should nevertheless refrain from targeting Saudi oil infrastructure, essentially respecting the truce concluded with Riyadh in 2022.

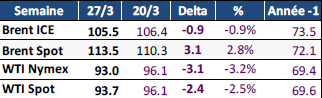

Over the week on average, the spot price of Brent stood at $113.5/bbl, up 2.8%, while WTI fell 2.5% to $93.7/bbl. On the futures markets, Brent for May delivery lost 1% to $105.5/bbl and WTI 3.2% to $93/bbl, a sign that the financial markets are counting on Donald Trump’s desire to quickly end the conflict. The Bloomberg consensus on March 27 raised its forecast for the average price of Brent in 2Q to $74.1/b (+$8.8/b) and to $68/b (+$2.2/b) in 3Q (figures 1 to 3). In the high scenario, the consensus now anticipates a price reaching $125/b in 2Q (+$15/b) and $96/b (+$5/b) in 3Q.

![]() Â Read more / Download the dashboard (PDF -Â 457 Ko)

Read more / Download the dashboard (PDF - 457 Ko)

Â

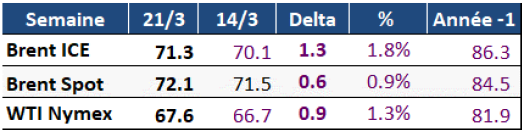

23 mars 2026

Brent crosses $112/bbl in a context of worsening conflict

Last week, oil prices rose dramatically, crossing the $112/bbl mark and reaching their highest level in almost four years. This outbreak takes place in a context of rapid deterioration of the geopolitical situation in the Middle East, marked by an Israeli attack against the Iranian gas installations in South Pars. In retaliation, Iran targeted several strategic energy infrastructures in the region, including the Samref refinery in Saudi Arabia, the Jubail petrochemical complex and the Ras Laffan gas site in Qatar. These attacks led to a surge in natural gas prices on the European market, which exceeded €60/MWh, a level without precedent for three years. Finally, the announcement of the deployment of American military reinforcements in the region and the ultimatum launched this weekend by American President Donald Trump, who threatened to “completely destroy” Iranian power plants if Tehran does not reopen not completely the Strait of Hormuz within 48 hours, further exacerbated tensions. In response, Tehran immediately threatened to carry out strikes against strategic energy infrastructure as well as seawater desalination facilities, which should increase the volatility of crude prices in the days to come.

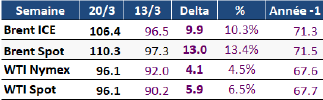

On a weekly average, the spot price of Brent stood at $110.3/bbl, up 13%, while that of WTI reached $96.1/bbl, up 6.5%. On the futures markets, Brent for May delivery rose 10% to $106.4/bbl, and WTI rose 4.5% to $96/bbl. The Bloomberg consensus, dated March 20, revised its forecasts for the average Brent price in 2Q to 65.3 /b (+0.3/b) and to $65.8/b (+$0.8/b) for 3Q (figures 1 to 3). The consensus high scenario now forecasts a price reaching $110/b in 2Q (+$20/b) and $90/b (+$4/b) in 3Q. Some scenarios envisage more pessimistic prospects. For example, in the event of a near-total blockage of the Strait of Hormuz, UBS anticipates a continued rise in the price of Brent, which could reach around $120/bbl by the end of March, before exceeding $150/bbl in 2Q 2026.

Market positioning data indicates that speculators currently hold the highest net buying volume in crude oil futures and options in a year. This figure constitutes a record since the start of 2025 in proportion of open contracts, and since 2021 in absolute volume of barrels. Despite this massive influx of speculative capital, the surge in oil prices far exceeds the influence of these financial flows alone. Anticipating imminent shortages, physical market players, such as refineries and importers, regained control of price formation. This dynamic is particularly visible in the refining margins of middle distillates, which are reaching historic levels.

![]() Â Read more / Download the dashboard (PDF -Â 460 Ko)

Read more / Download the dashboard (PDF - 460 Ko)

Â

16 mars 2026

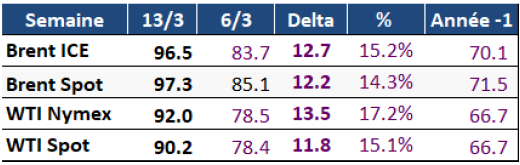

Faced with a bogged-down conflict, Brent rises to more than $100/bbl

The oil market opened last week sharply higher, with Brent approaching $120/bbl, before temporarily falling back to $90/bbl, following President Donald Trump’s announcement of a rapid end to the conflict.

Prices then resumed their progression to reach $103.1/bbl at Friday’s close, driven by intensifying fighting, attacks on oil infrastructure and the persistent blockage of the Strait of Hormuz, a sign that the conflict is getting bogged down and could last longer than initially expected.

Market attention remains mainly focused on the almost complete blockage of the Strait of Hormuz, which removes around 15 Mb/d from global supply, representing a cumulative loss to date of more than 250 Mb, an unsustainable rate in the medium term for the world economy. To limit tensions, IEA members decided to release 400 million barrels from their strategic reserves. However, in the absence of a resumption of maritime traffic in the Strait of Hormuz, this measure will not be enough to sustainably stabilize oil prices.

On a weekly average, oil prices have increased significantly. The spot price of Brent stood at $97.3/bbl, up 14%, while that of WTI reached $90.2/bbl, up 15%. On the futures markets, the Brent contract for delivery in May increased by 15%, to $96.5/bbl, and WTI by 17%, to $92/bbl.

Market expectations are also on the rise. The Bloomberg consensus of March 13 revises the expected average price of Brent to $65/bbl in 2026, an increase of $1.6/bbl (see figures 1 to 3). The consensus high scenario now reaches $90/bbl in the second quarter (+$5/bbl) and $86/bbl in the third quarter. In the various analyzes published in recent days, the hypothesis of a conflict lasting approximately one month tends to emerge as the basic scenario, even if some suggest a conflict which could last up to three months. According to Natixis, a one-month supply interruption, fully compensated by a draw on stocks in OECD countries, would imply an equilibrium Brent price of around $99/bbl, excluding the geopolitical risk premium. A three-month interruption could push this level up to $178/bbl.

To limit the impact of the war on energy prices and consumers, several measures have been put in place on a global scale. China has ordered an immediate ban on exports of refined petroleum products. Japan and South Korea introduced subsidies and price caps to protect consumers, while Australia eased fuel standards to make more gasoline available. In the United States, a temporary exemption from the Jones Act is being considered to facilitate domestic shipping. The European Union is considering reducing or suspending emissions-related costs to reduce electricity prices. Despite these initiatives, the effects are already being felt, with pump prices and plane tickets rising sharply, as well as extreme situations, such as in India where some hotels are rationing LPG, or in Pakistan and Bangladesh, which have introduced more general fuel rationing.

![]() Â Read more / Download the dashboard (PDF -Â 600 Ko)

Read more / Download the dashboard (PDF - 600 Ko)

Â

9 mars 2026

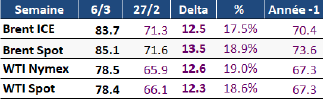

United States – Israel – Iran War: After a week of conflict, oil markets under high tension

A week after the start of hostilities between the United States, Israel and Iran, the conflict intensified and spread throughout the region, including southern Lebanon where Israel launched a reprisal operation against the Hezbollah at the end of the week. During the week, reports of attacks on energy infrastructure multiplied, propelling Brent to nearly $93/bbl at the end of the week, then to more than $115/bbl this morning, when the markets opened. Strikes notably affected several strategic oil infrastructures: the surroundings of the Ras Tanura refinery in Saudi Arabia, the Kharg island terminal, the Bahrain refinery (which declared force majeure), the port of Fujairah, as well as several oil depots in Iran. As a precautionary measure, several countries, including Qatar, Israel, Saudi Arabia and the United Arab Emirates, have carried out a preventive shutdown of part of their energy installations.

At the same time, Iran maintains an almost total blockade of the Strait of Hormuz and threatens to strike any ship that attempts to cross it. Such a situation, unprecedented in the history of this strategic sea route, fuels fears of a major energy shock on the markets, if it were to continue. The blockage of the strait for several weeks is now considered a basic scenario by analysts. Faced with this prospect, Donald Trump announced that the US Navy could, if necessary, escort oil tankers across the Strait. He also ordered the establishment of political risk insurance mechanisms and financial guarantees for maritime trade in the Gulf of Oman. But for the moment, no oil tanker is taking the risk of venturing there, in the face of Iranian threats.

On a weekly average, the spot price of Brent increased by 18.9% to reach $85.1/bbl, while that of WTI increased by 18.6% to settle at $78.4/bbl. The Bloomberg consensus of March 4 is also up sharply, with a Brent price estimated at $65/b (+$1/b) for the first quarter and $63.3/b (+$0.5/b) for the year 2026 (fig. 1 to 3). The Bloomberg consensus high scenario now reaches $85/bbl for the second and third quarters of the year, an increase of $11/bbl compared to last week.

![]() Â Read more / Download the dashboard (PDF -Â 340 Ko)

Read more / Download the dashboard (PDF - 340 Ko)

Â

02 mars 2026

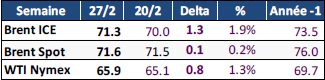

American and Israeli strikes against Iran: strong fears of disruptions to oil and gas flows and upward pressure on prices

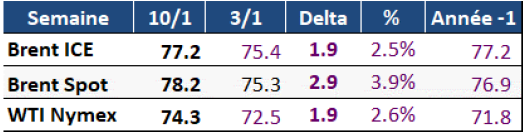

Last week, while discussions between the United States and Iran continued on nuclear power and the market remained tense by the risk of a military escalation, the price of Brent closed Friday at $72.5 per barrel, reflecting the strong geopolitical risk premium incorporated by market players. On a weekly average, Brent rose 1.9% to $71.3/bbl, while WTI rose 1.3% to $65.9/bbl. The Bloomberg consensus of February 26 is also up sharply, with a Brent price estimated at $64/b (+$3/b) for the first quarter and $62.9/b (+$1.5/b) for the year 2026 (fig. 1 to 3).

![]() Â Read more / Download the dashboard (PDF -Â 615 Ko)

Read more / Download the dashboard (PDF - 615 Ko)

Â

23 February 2026

Faced with the growing threat of conflict between the United States and Iran, Brent rises to $70/bbl

Last Wednesday, oil prices rose sharply, recording an increase of more than 4%, in a context of renewed geopolitical tensions in the Middle East and the stagnation of the Russian-Ukrainian conflict. This upward dynamic was accentuated following press reports according to which Israel had raised its alert level in the face of the prospect of an American or Israeli strike against Iran. At the same time, Iranian media announced joint naval exercises with Russia in the Arabian Sea and the northern Indian Ocean, while Tehran temporarily closed certain areas of the Strait of Hormuz, a strategic crossing point for global oil trade.

Analysts now believe that it is not insignificant that the United States will take military action against Iran in the coming weeks, which contributes to increasing market volatility. The OVX, an index of the 30-day implied volatility of the WTI oil price often referred to as the “oil fear index”, reached its highest level since June 2025, signaling significant investor concern (fig. 10). Another indicator of these tensions: maritime freight rates have increased sharply, with the Baltic index for oil tankers peaking at 1,787 points, the highest level since the end of 2022 (fig. 11). If officially the United States maintains a hard line (“zero enrichment” on Iranian soil), the Trump administration would be ready to study a proposal allowing Iran to maintain limited nuclear enrichment, provided that it is impossible for Tehran to derive one. military capacity. The question is therefore whether this diplomatic opening will be enough to avoid a direct confrontation, while military preparations are intensifying on both sides, with the arrival of a new American aircraft carrier in the Mediterranean.

![]() Â Read more / Download the dashboard (PDF -Â 325 Ko)

Read more / Download the dashboard (PDF - 325 Ko)

Â

16 February 2026

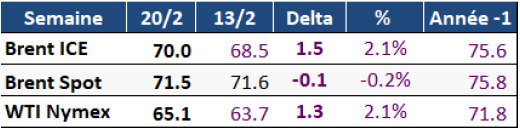

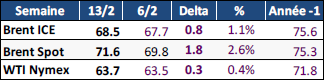

At €68.5/bbl, Brent remains supported by still significant geopolitical risks

Last week, oil prices were supported at the start of the period by the persistence of geopolitical tensions in the Middle East, particularly after a warning from the United States regarding navigation in the Strait of Hormuz. By mid-week, however, prices fell by around $2/bbl. This decline results from a combination of both geopolitical and structural factors. On the geopolitical level, the opening this week in Geneva of a new round of negotiations between the United States and Iran on the nuclear issue helped to ease immediate tensions linked to Iran, thus reducing the risk premium on the markets oil tankers. On the supply side, several sources indicate that OPEC+ would consider resuming its production increases from April, a decision which could be made official at the March 1 meeting. Furthermore, the Trump administration accelerated the issuance of waivers from sanctions targeting Venezuela, facilitating the return of investments in the oil sector and opening the prospect of a restoration of production levels before the blockade from the second quarter of the year (around 1 Mb/d). Finally, the latest monthly report from the International Energy Agency confirmed lower-than-anticipated growth in global demand for this year, as well as a significant excess supply. These elements, combined with a sharp increase in weekly oil stocks in the United States, reinforced the downward pressure on crude prices.

Over the week, Brent for May delivery rose 1.1% to $68.5/bbl, while WTI edged up 0.4% to $63.7/bbl. The Bloomberg consensus of February 13 is stable, with a Brent price estimated at $61/bbl for the first quarter. Market positioning data shows that speculative positions remained broadly stable over the past week but still at a significantly elevated level compared to that observed over the past year, which maintains a downward risk bias. (Fig. 1 to 3)

![]() Â Read more / Download the dashboard (PDF -Â 324 Ko)

Read more / Download the dashboard (PDF - 324 Ko)

Â

9 February 2026

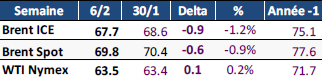

After 4 weeks of weekly increases, Brent falls, but the geopolitical premium remains high

Last week, oil prices were very volatile, mainly driven by tensions between the United States and Iran, as well as discussions around the Iranian nuclear program. The markets went from the hope of appeasement to the fear of an escalation, reacting strongly to each diplomatic or military announcement in the region.

In addition to these geopolitical tensions, several structural factors have influenced the evolution of oil prices. OPEC+ first confirmed the maintenance of its production for the month of March, an expected decision which helped to stabilize market expectations. At the same time, the United States recorded an unexpected drop in its crude stocks, with a drop of 3.5 million barrels, which reinforced the upward pressure on prices. Another major event marked the week: the conclusion of a trade agreement between Washington and New Delhi. The United States has agreed to reduce customs duties on certain Indian products in exchange for India’s commitment to stop its purchases of Russian oil, a measure which is also part of the tightening of sanctions against Russia. This agreement could ultimately reshape global oil supply flows. Finally, Saudi Arabia lowered the price of its Arabian Light crude for Asian buyers to its lowest level since 2021 compared to the average Oman/Duba price, confirming that the market remains in a situation of excess supply.

Over the week, Brent for April delivery fell 1.2% to $67.7/bbl, while WTI edged up 0.2% to $63.5/bbl. The Bloomberg consensus of February 6 was revised upwards, with a Brent price estimated at $61/bbl for the first quarter. Finally, positioning data shows that speculators continued to massively buy oil contracts. The weight of speculative positions on Brent and WTI reached its highest level since September, a sign of a market very dominated by bullish speculators (Fig. 10). In this context, analysts now believe that speculative flows should continue to weigh on crude prices overall, but with more limited upside potential and an increased risk of rapid downward corrections, except in the event of a new major geopolitical event.

![]() Â Read more / Download the dashboard (PDF -Â 347 Ko)

Read more / Download the dashboard (PDF - 347 Ko)

Â

2 February 2026

Iranian risk pushes Brent to more than $70/bbl

Oil prices rose sharply last week, reaching their highest level in six months on Thursday. This increase is mainly explained by geopolitical tensions between the United States and Iran, which currently dominate the market.

Statements by US President Donald Trump, speaking of possible targeted military strikes against Tehran, have revived fears of a major disruption in oil supply. These concerns have been reinforced by military movements and the announcement of new American and European sanctions targeting Iran. The main risk for the markets remains a regional escalation likely to affect oil flows, in particular via the Strait of Hormuz through which nearly 20 Mb/d pass.

If Washington and Tehran gave a glimpse at the end of the week of a possible resumption of dialogue, uncertainty remains high. This weekend, the Iranian Foreign Ministry nevertheless expressed its hope of avoiding a conflict, and discussions between the two countries could open in the coming days. In this context of relative calm, the price of Brent fell sharply this morning, down around 6%, returning to around $66/bbl.

Other factors, although secondary, also supported prices: an unexpected drop in US inventories, temporary production disruptions in the United States linked to the winter storm, as well as difficulties at the giant Tengiz oil field, in Kazakhstan (0.9 Mb/d), and at the CPC terminal, even if a gradual recovery is expected. Added to this was a decline in the US dollar at the start of the week, with the euro briefly crossing the $1.2 threshold for the first time in more than four years, which made oil more attractive to buyers outside the dollar zone and mechanically supported prices.

![]() Â Read more / Download the dashboard (PDF -Â 300 Ko)

Read more / Download the dashboard (PDF - 300 Ko)

Â

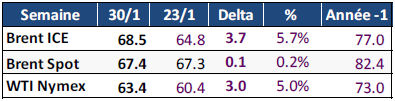

January 26, 2026

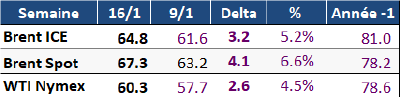

Fundamentals compensate for geopolitical risk. Brent stable at $64.8/bbl

After a rather calm start to the week, marked by a more conciliatory speech from Donald Trump towards Europe during the Davos Forum and by the publication of the monthly report from the International Energy Agency (IEA) confirming the persistence of an oil supply surplus, oil prices finally closed the week with a strong increase (+2.8% for Brent). This progression can be explained by several factors: the persistent drop in production in Kazakhstan, the arrival of a major winter storm in North America and the ever-present Iranian risk, particularly volatile, revived by the deployment of an imposing fleet of American warships towards Iran.

At the same time, markets continued to factor in several bearish factors. These include prospects for a possible peace deal in Ukraine, the gradual increase in Venezuelan exports under US-backed deals, and rising US crude oil inventories.

Over the week, Brent for March delivery rose 0.1% to $64.8/bbl, while WTI gained 0.1% to $60.4/bbl. The Bloomberg consensus of January 23 is stable with a Brent price of $60/bbl in the first half (fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 300 Ko)

Read more / Download the dashboard (PDF - 300 Ko)

Â

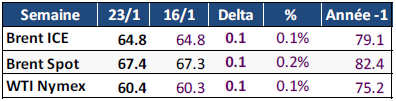

January 19, 2026

The possibility of American intervention in Iran pushes Brent to nearly $67/bbl

Last week, oil prices were strongly influenced by tensions in Iran and Donald Trump’s threats against the Tehran regime. These events propelled the price of Brent to nearly $67/bbl, its highest level since the beginning of October (fig. 1&2). However, the US president’s statements mid-week, in which he spoke of an end to the killings in Iran, temporarily allayed fears of US military intervention, leading to a drop of around $3/bbl in the price of crude. Despite this lull, the risk of an escalation persists and continues to weigh on the markets.

Market concerns are not so much about a possible drop in Iranian exports. Iran, the fifth largest producer in OPEC+, extracts around 3.5 Mb/d, of which 1.9 Mb/d is exported, mainly to China. The main risk lies rather in the possibility of a blockage of the Strait of Hormuz, a strategic crossing point through which nearly a quarter of the world’s maritime oil passes.

If the situation in Iran calms down, the markets’ attention could turn again to Venezuela. A gradual return of volumes recently sanctioned or blocked could in fact revive fears of an excess of supply on the oil market in 2026, as highlighted by the EIA in its latest monthly report. The key question remains whether this excess oil will actually reach global markets. In 2025, the oil surplus was mainly absorbed by China to replenish its strategic reserves, unlike OECD countries whose stocks remained stable. If, in the future, a larger share of this overproduction were directed to industrialized countries, particularly in the event of a slowdown in Chinese purchases, prices could come under significant downward pressure. The EIA thus anticipates an average Brent price of $56/bbl in 2026 then $54/bbl in 2027. In the short term, however, the risk premium linked to threats to supply should continue to support prices.

Over the week, Brent for March delivery rose 5.2% to $64.8/bbl, while WTI gained 4.5% to $60.3/bbl. The Bloomberg consensus of January 16 is stable with a Brent price of $60/bbl in the first half (fig. 3). On the futures markets, institutional investors significantly increased their speculative upward positions on Brent, bringing their commitments to 208,461 contracts last week, up +70%, their highest level in nine months. This dynamic suggests an anticipation of a rebound in prices in a geopolitical context that remains tense, despite a market context marked by abundant stocks and excess supply.

![]() Â Read more / Download the dashboard (PDF -Â 307 Ko)

Read more / Download the dashboard (PDF - 307 Ko)

Â

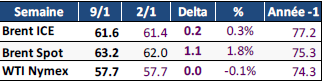

January 12, 2026

Brent rises with uncertainty in Venezuela and tensions in Iran

Oil prices rose this week as investors tried to gauge the impact of numerous

statements by the American administration regarding the management of Venezuelan oil. At the same time, supply tensions have increased on several fronts. An oil tanker bound for Russia was the target of a drone attack in the Black Sea, while Ukraine claimed strikes against three oil production platforms in the Caspian Sea. At the same time, Iraq resumed exploitation of the West Qurna field, one of the largest in the world, after the imposition of American sanctions against Lukoil. Finally, the intensification of demonstrations in Iran has revived market concerns, which fear that the lasting deterioration of the situation in one of the world’s main producing countries, with production of around 3.5 Mb/d last November, will affect crude production and exports.

Over the week, Brent for March delivery rose 0.3% to $61.6/bbl, while WTI lost 0.1% to $57.7/bbl. The Bloomberg consensus of January 9 is stable with a Brent price of $60/bbl in the first half (fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 329 Ko)

Read more / Download the dashboard (PDF - 329 Ko)

Â

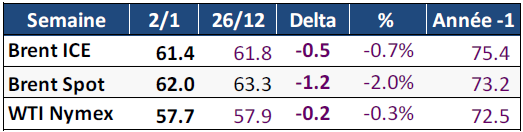

January 5, 2026

Brent falling while waiting to see more clearly on the situation in Venezuela

Oil prices fell slightly during the first trading session of 2026, extending the significant losses recorded last year, as investors continue to trade off between lingering fears of a supply glut and geopolitical risks high.

The markets began the year cautiously, after Brent and WTI recorded their biggest annual decline since 2020 in 2025. Despite a tense geopolitical context, price developments indicate that operators are focusing above all on fundamentals, in particular on the prospect of lastingly abundant global supply.

The escalation of tensions between Venezuela and the United States reached its peak last Saturday, with strikes carried out by American forces and the arrest of President Nicolás Maduro. This intervention is part of an assumed reaffirmation of the Monroe Doctrine, which considers Latin America as falling within Washington’s sphere of strategic influence. The declared desire of the United States to “steer” or “supervise” the Venezuelan democratization process nevertheless raises numerous questions, both on its modalities and on its real objectives.

Several scenarios are now possible, ranging from limited military support intended to secure a political transition to the establishment of a provisional government supported by the United States. The outcome of this sequence will be decisive for the country’s economic prospects, in particular for the oil sector, a historic pillar of the Venezuelan economy and at the heart of the ambitions of Donald Trump, who wishes to encourage the return of the American oil majors.

While a favorable scenario could unlock significant economic recovery potential, this reaffirmation of the Monroe Doctrine also carries high risks of prolonged instability and negative reactions at the regional level. It could reignite tensions with certain Latin American countries and accentuate strategic rivalry with China and Russia, both of which hold some of the country’s largest oil concessions (4.4 Gb and 2.3 Gb respectively), thus drawing a fragile balance between economic opportunities and risks geopolitics.

Over the week, Brent for March delivery fell 0.7% to $61.4/bbl, while WTI lost 0.3% to $57.7/bbl. According to the Bloomberg consensus of January 2, the price of Brent should settle at $60.3/bbl in 2026 (fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 325 Ko)

Read more / Download the dashboard (PDF - 325 Ko)

Â

2025

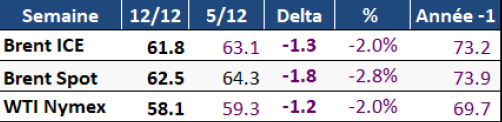

December 15, 2025

Brent falls in the face of weak fundamentals

Crude oil prices fell last week, despite a still tense geopolitical context, both in Ukraine and off the Venezuelan coast after the seizure of an oil tanker by the American authorities. The weakness of the physical market continues to weigh on prices, which have lost more than 18% since the start of the year (fig. 1 & 2). The sharp increase in American stocks of gasoline and distillates observed last week thus confirmed the situation of excess supply highlighted in the latest forecasts from the IEA and the EIA. Finally, the weakening of the dollar, following the decision of the Federal Reserve to lower its key rates, also reinforced the downward pressure (fig.13).

Over the week, Brent for January delivery fell 2% to $61.8/bbl, while WTI lost 2.0% to $58.1/bbl. The Bloomberg consensus of December 12 remains stable, with a Brent price of $63/bbl for the fourth quarter of 2025 and $60.7/bbl for the first quarter of 2026. As an annual average for 2026, the consensus is $61.8/bbl (fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 340 Ko)

Read more / Download the dashboard (PDF - 340 Ko)

Â

December 8, 2025

Brent stable supported by the improvement in the macroeconomic context and persistent geopolitical tensions

The price of Brent changed little this week, supported by the improvement in the macroeconomic context and persistent geopolitical tensions. However, the oil market remains dominated by structural uncertainty linked to the prospect of excess supply in 2026. The combination of high geopolitical risk and anticipated excess supply creates a nervous and capped market, where any increase remains fragile and dependent on external signals, whether diplomatic, monetary or geopolitical.

The price of Brent changed little this week, supported by the improvement in the macroeconomic context and persistent geopolitical tensions. However, the oil market remains dominated by structural uncertainty linked to the prospect of excess supply in 2026. The combination of high geopolitical risk and anticipated excess supply creates a nervous and capped market, where any increase remains fragile and dependent on external signals, whether diplomatic, monetary or geopolitical.

This week, the publication of new forecasts from major energy agencies should once again weigh on oil prices. Although no major revision is expected, these reports should confirm that supply will remain significantly in excess for the coming year. In this context, Saudi Aramco lowered all its official selling prices (OSP) to Asia for January cargoes. The Arab Light premium over the regional benchmark price was reduced to $0.60/bbl, its lowest level since January 2021. Price differentials granted to US and European refiners were also reduced. reduced, to $2.50/b and $0.05/b respectively. These adjustments are clearly part of Saudi Arabia’s strategy, which seeks to support oil prices in a market marked by excess supply. They also demonstrate Riyadh’s desire to defend its market shares, mainly in Asia, where competition remains keen, particularly in the face of Russian barrels sold at low prices.

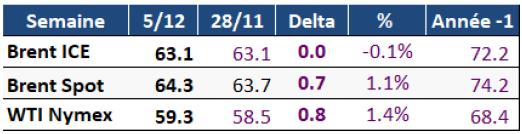

Over the week, Brent for January delivery fell 0.1% to $63.1/bbl, while WTI gained 1.4% to $59.3/bbl. The Bloomberg consensus of December 5 remains stable, forecasting a Brent price of $63/bbl for the fourth quarter of 2025 and $60.7/bbl for the first quarter of 2026. As an annual average for 2026, the consensus is $61.8/bbl (fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 325 Ko)

Read more / Download the dashboard (PDF - 325 Ko)

Â

December 1,

Brent falls slightly: the hope of a possible easing of the conflict in Ukraine continues to exert moderate downward pressure on prices

Oil prices remain in a range of $60 to $65/bbl, where they have been moving steadily since the beginning of October, despite Ukrainian attacks targeting two tankers from the Russian ghost fleet and an attack on the oil terminal of the CPC consortium, which provides most of Kazakhstan’s crude exports. to the Black Sea via Russia.

Oil prices remain in a range of $60 to $65/bbl, where they have been moving steadily since the beginning of October, despite Ukrainian attacks targeting two tankers from the Russian ghost fleet and an attack on the oil terminal of the CPC consortium, which provides most of Kazakhstan’s crude exports. to the Black Sea via Russia.

The hope of an easing of the conflict in Ukraine continues to exert moderate downward pressure on prices.

At the same time, the biannual OPEC+ meeting which was held this weekend had no effect on prices, due to a lack of specific expectations: the production levels of member countries were already fixed until December 2026, no significant new announcements were anticipated.

Over the week, Brent for January delivery fell 1% to $63.1/bbl, while WTI lost 1.6% to $58.5/bbl. On a monthly average, Brent posted a decline for the second consecutive month, to $63.7/bbl, a decrease of 0.5% compared to October. Since the start of the year, the price of Brent has fallen by more than 18%. The Bloomberg consensus of November 24 remains stable, forecasting a Brent price of $63/bbl for the fourth quarter of 2025 and $60.7/bbl for the first quarter of 2026. As an annual average for 2026, the consensus is $61.5/bbl (fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 330 Ko)

Read more / Download the dashboard (PDF - 330 Ko)

Â

November 24, 2025

Brent falls slightly as US sanctions against Russian oil come into effect

Oil prices changed little last week, caught between two opposing tensions: on the one hand, the entry into force of American sanctions targeting in particular the Russian giants Lukoil and Rosneft is fueling fears of disruptions in global supplies; on the other, the prospects of a structural surplus in supply by 2026 persist, while OPEC+ plans to increase its production by 137 kb/d in December.

At the end of the week, however, crude prices fell: Brent lost more than 1% and WTI almost 2%. This drop follows the announcement of an American diplomatic initiative aimed at promoting a peace plan in Ukraine. If the possibility of a de-escalation remains very uncertain, the markets immediately anticipated a return of additional volumes of Russian oil on the international scene. This prospect was enough to exert downward pressure on prices, illustrating the persistent sensitivity of investors to geopolitical developments likely to modify the global balance between supply and demand for oil.

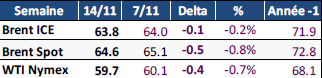

Over the week, Brent for January delivery fell 0.3% to $63.7/bbl, while WTI lost 0.4% to $59.5/bbl. The Bloomberg consensus of November 19 is stable, with Brent at $63/b in the fourth quarter of 2025 and $60.7/b (- $0.2/b) in the first quarter of 2026. On average for the year 2026, the Bloomberg consensus is $61.5/b (Fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 313 Ko)

Read more / Download the dashboard (PDF - 313 Ko)

Â

November 17, 2025

Brent down to $64/bbl supported by geopolitical tensions, capped by fundamentals

Brent continues to oscillate between $63 and $65/bbl, supported by geopolitical tensions, but capped by fundamentals (Fig. 1 & 2). Prices fell suddenly in the middle of the week, with the publication of monthly agency reports and the announcement of an even greater surplus of supply than anticipated by the IEA. They then increased sharply, after a Ukrainian attack by missiles and drones against the port of Novorossiysk, the leading Russian port in terms of traffic. At the same time, the sanctions imposed by Washington on Russia, and on Rosneft and Lukoil in particular, continue to complicate Russian exports, a large part of which is currently stored on tankers (Fig. 15), with traders facing payment and delivery obstacles as the November 21 deadline approaches. Lukoil’s declaration of force majeure on the Iraqi West Qurna-2 oil field is, at this stage, the most visible consequence of the sanctions.

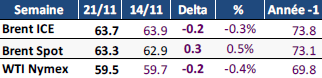

Over the week, Brent for January delivery fell 0.2% to $63.8/bbl, while WTI lost 0.7% to settle at $59.7/bbl. The Bloomberg consensus of November 14 is almost unchanged, with Brent at $63/b in the fourth quarter of 2025 and at $60.7/b (- $0.2/b) in the first quarter of 2026. On average for the year 2026, the Bloomberg consensus is $61.5/b (Fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 390 Ko)

Read more / Download the dashboard (PDF - 390 Ko)

Â

November 10, 2025

Brent stable at $64/bbl but fears of a global supply surplus remain

Crude oil prices remained relatively stable last week, with Brent oscillating between $64 and $65/bbl. Despite OPEC+’s decision to suspend any further increase in production in the first quarter of 2026, after an increase of 137 kb/d planned for December, fears of a global supply surplus remain.

On the economic level, the signals remain fragile. In Asia as in the United States, manufacturing indicators continue to decline, with American industrial activity even recording an eighth consecutive month of contraction.

Furthermore, the uncertainties linked to the monetary policy of the Federal Reserve encourage investors to be cautious.

Although the Fed recently lowered its rates, several of its officials reiterated that a rapid easing cycle was not envisaged, thus fueling fears of a prolonged slowdown in global growth. Finally, the strength of the US dollar, which reached a four-month high, is weighing on oil prices.

Despite this gloomy context, the market benefits from a few supporting factors. Chinese imports of crude oil increased by 8.2% year-on-year in October, reflecting the dynamism of local refineries. Additionally, disruptions linked to sanctions against Russia continue to limit some flows to China and India, which provides one-off price support. Analysts are divided as to the medium-term trajectory: some anticipate Brent at $50/bbl at the end of 2026, counting on a sustainable excess supply, while others, more optimistic, are betting on a

stabilization around $60/bbl.

![]() Â Read more / Download the dashboard (PDF -Â 330 Ko)

Read more / Download the dashboard (PDF - 330 Ko)

Â

03 November 2025

Oil: prices without clear direction between growing supply and uncertain demand

After the strong market reaction to the announcement of new US sanctions against Russia, crude oil prices moved without a clear trend last week. Torn between the anticipation of an increase in OPEC+ production and contradictory signals regarding global demand, Brent and WTI fell slightly to close at around $65 and $61/bbl, after several volatile sessions.

On the geopolitical level, tensions remain despite a certain calming down. The meeting between Donald Trump and Xi Jinping resulted in a limited trade agreement providing for a partial reduction in customs duties and the resumption of certain Chinese imports of American products, particularly in the energy sector. This truce briefly supported the markets, but did not allay concerns linked to the slowdown in the global economy. Furthermore, speculation about possible American military action in Venezuela, quickly denied, caused a brief rebound in prices. Finally, the rise of the dollar to its highest level in almost three months, following the Fed’s rate cut, exerted slight downward pressure on oil prices.

Over the week, Brent for December delivery rose 2.6% to $65/bbl, while WTI gained 2.1% to $60.7/bbl. On the futures markets, net long positions in Brent rebounded strongly, with an increase equivalent to 119 million barrels, the third fastest ever recorded (fig. 10). This movement reflects a return to a more neutral position on the part of investors, after a period marked by strong pessimism, reflecting uncertainty as to the real impact of American sanctions on Russian exports and the extent of the excess supply expected for next year.

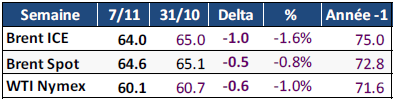

Bloomberg’s October 31 forecast remains cautious, anticipating a Brent price of $63/bbl in the fourth quarter of 2025, then $61.5/bbl (+$0.5/bbl) in the first quarter of 2026. The month of October ends with a monthly decline of around 5% for Brent and WTI, at 64.0 and $60.1/bbl on average. Since the start of the year, Brent has fallen by 18%, confirming the underlying trend of an overabundant market, but vulnerable to geopolitical upheavals and fluctuations in demand.

![]() Â Read more / Download the dashboard (PDF -Â 327 Ko)

Read more / Download the dashboard (PDF - 327 Ko)

Â

October 27, 2025

American sanctions against Russia shake the market: Brent starts to rise again

Last week, oil prices rebounded strongly, erasing in just two days the declines accumulated over the previous three weeks, linked to fears of record overproduction. This turnaround is mainly explained by the tightening of American sanctions against Russia, targeting the oil giants Rosneft and Lukoil. The announcement caused an immediate rise in crude prices: Brent gained 5.4% to $66/bbl and WTI 5.6% to $61.8/bbl, recording their biggest daily increase since June. However, traders remain cautious, the effectiveness of the long-term sanctions is uncertain, their impact depending on the reaction of the main buyers, notably China and India, as well as the ability of OPEC+ to adjust its production to compensate for possible drops in Russian supply. These questions led to a slight decline in prices at the close last Friday.

On the futures markets, the announcement of the sanctions led to a reversal of the price structure, with a return to marked backwardation, a sign of a market once again under tension in the short term. Over the week, Brent for December delivery rose 2.2% to $63.4/bbl, while WTI gained 2.0% to $59.4/bbl. The sharp drop in the price differential between Brent and Dubai since the announcement of the sanctions (fig. 12) also shows that some buyers are actively looking for alternative crude oil grades, particularly in the Middle East.

Bloomberg’s October 24 forecasts remain cautious, anticipating Brent at $63/bbl in the fourth quarter of 2025, then at $61/bbl in the first quarter of 2026. In this context, the meeting between Donald Trump and Xi Jinping, scheduled for this week, is crucial, both for trade agreements likely to revive global economic growth and for assess China’s position in the face of US sanctions against Russia.

![]() Â Read more / Download the dashboard (PDF -Â 345 Ko)

Read more / Download the dashboard (PDF - 345 Ko)

Â

October 20, 2025

Brent in decline, the IEA anticipates an unprecedented oil surplus in 2026

For the third consecutive week, oil prices fell, reaching their lowest level in five months. This decline is mainly explained by the publication of the monthly report from the International Energy Agency (IEA), which anticipates a record overproduction of 4 Mb/d in 2026. Trade tensions between Washington and Beijing are also fueling downward pressure on oil prices by reviving fears of a global economic slowdown, even if the two countries have expressed their desire to quickly relaunch their discussions. Finally, the geopolitical détente linked to the ceasefire in the Gaza Strip also contributed to reducing the risk premium integrated into crude prices. In this context, Russian oil exports remain today the main factor supporting crude prices. At the end of the week, a declaration by President Trump according to which India had agreed to stop its purchases of Russian oil briefly caused Brent prices to rebound (fig. 1 and 2). If this information is confirmed, New Delhi would have to turn to other suppliers, which would tighten the supply of non-Russian crude. However, Indian authorities have not yet confirmed this announcement.

![]() Â Read more / Download the dashboard (PDF -Â 340 Ko)

Read more / Download the dashboard (PDF - 340 Ko)

Â

October 13, 2025

Brent falls sharply with the return of trade tensions between China and the United States

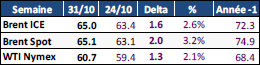

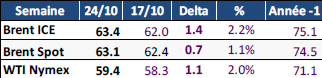

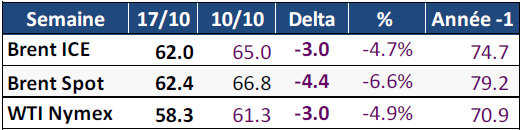

Oil prices fell sharply last week, erasing the gains recorded at the start of the period, against a backdrop of economic uncertainties and renewed trade tensions between China and the United States. After an initial rebound, driven by OPEC+’s decision to contain the production increase to 137 kb/d for November, Brent reached a temporary peak close to $67/b on Wednesday. But the trend quickly reversed at the end of the week. Beijing’s announcement of new restrictions on exports of rare earths, followed by Donald Trump’s threats to impose 100% customs duties on Chinese products, caused a wave of sales across all commodity markets. At the same time, the increase in oil stocks in the United States, the publication of the monthly EIA report which anticipates a structural surplus in supply until 2026, as well as the drop in Chinese crude imports, have reinforced the downward pressure on prices.

On a weekly average, Brent for delivery in December lost $0.8/bbl (-1.2%), to settle at $65.0/bbl, while WTI lost $0.5/bbl (-0.8%), to reach $61.3/bbl (fig. 2). According to the Bloomberg consensus of October 10, the price of Brent should remain stable at $63/bbl in the fourth quarter of 2023 (see Figure 3) and at $61/bbl in the first quarter of 2026.

![]() Â Read more / Download the dashboard (PDF -Â 332 Ko)

Read more / Download the dashboard (PDF - 332 Ko)

Â

October 06, 2025

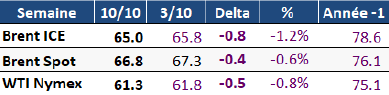

Brent falls sharply before the OPEC+ meeting

Crude prices fell sharply last week, as market players anticipated this weekend’s OPEC+ decision to increase production for the month of November, thus rekindling fears of an excess supply next year (fig. 1 and 2). Several factors accentuated this downward movement: the resumption of crude exports via Turkey after a two and a half year interruption, the partial closure of the American federal administrations against a backdrop of budgetary impasse, as well as the publication of data revealing an increase in oil and gasoline stocks in United States more marked than expected. Added to this were press reports reporting cargoes of crude from the Middle East, notably the United Arab Emirates and Qatar, remaining without buyers, a signal perceived as the first tangible indication of excess supply.

In this context, some analysts estimate that the OPEC+ decision, combined with IEA forecasts anticipating a supply surplus of 3.3 Mb/d in 2026, could bring Brent back to $50/b as early as next year. However, the futures markets are currently charting a different trajectory: 12- and 24-month contracts are currently trading around $64/bbl, close to current prices.

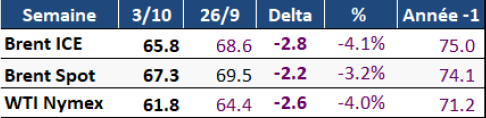

On a weekly average, Brent for delivery in November lost $2.8/b (-4.1%), to settle at $65.8/b, while WTI lost $2.6/b (-2.6%), to reach $61.8/b (fig. 2). The Bloomberg consensus of October 3 for the price of Brent is stable at $63/bbl in the fourth quarter (fig. 3) and $61/bbl in the first quarter of 2026.

![]() Â Read more / Download the dashboard (PDF -Â 324 Ko)

Read more / Download the dashboard (PDF - 324 Ko)

Â

September 29, 2025

Brent exceeds $70/bbl with intensifying tensions between Russia, Ukraine and NATO and OPEC+ production below expectations

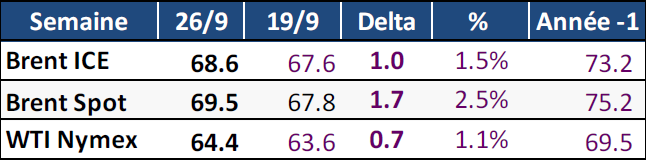

Rising geopolitical risks, renewed concerns over Russian supplies due to Ukrainian drone attacks on oil infrastructure and excess speculative positions on the downside triggered the largest weekly rise in oil prices last week since the war between Iran and Israel in June. Over the week, prices increased by more than $3/bbl and Brent crossed the $70/bbl threshold for the first time since July (fig. 1&2). Data on market positions confirmed that speculators were net sellers of oil until last Tuesday and that net positions remained strongly oriented downward, which explains in reaction the rise in the price of crude oil with the intensification of tensions between Russia, Ukraine and NATO. On a weekly average, Brent for November delivery gained $1/bbl (+1.5%), to settle at $68.6/bbl, while WTI gained $0.7/bbl (+1.1%), to reach $64.4/bbl (fig. 2). The Bloomberg consensus of September 26 for the price of Brent is stable at $66/bbl in the third quarter and $63/bbl in the fourth quarter (fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 315 Ko)

Read more / Download the dashboard (PDF - 315 Ko)

Â

September 22, 2025

Brent up to $67.6/bbl amid geopolitical tensions and new European sanctions against Russia

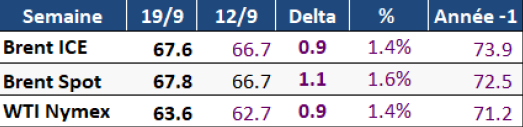

The oil market continues to evolve in a context of persistent geopolitical tensions and the prospect of new European sanctions against Russia. Ukrainian attacks on Russian energy infrastructure early last week knocked out more than 6% of the country’s refining capacity and disrupted operations at the strategic Primorsk terminal, potentially limiting exports and creating a floor price for crude. At the same time, the American Federal Reserve lowered its key rate by 25 basis points and announced that it was considering a gradual easing by the end of the year. This orientation could, in the long term, support energy demand, even if American economic indicators, particularly in employment and real estate, continue to signal a slowdown in economic activity. On the supply side, the resumption of Kazakh flows via the BTC oil pipeline and the lifting of restrictions on Nigerian terminals have helped to rebalance the global market.

On Friday, as expected, the European Commission presented its 19th package of sanctions against Russia. The new package includes penalties for traders, refineries and petrochemical companies from third countries, including China, that violate existing rules on Russian energy imports.

The proposal also includes the inclusion of 118 ships belonging to the Russian “ghost fleet” on the list of sanctioned ships. Furthermore, the European Union is considering bringing forward the ban on imports of Russian liquefied natural gas (LNG) by one year, with implementation potentially set for January 1, 2027. The American administration has publicly supported these initiatives. Donald Trump called on the EU to introduce heavy customs duties targeting the main buyers of Russian oil, such as China and India, and to accelerate its exit from energy dependence on Moscow.

On a weekly average, Brent for delivery in November gained $0.9/bbl (+1.4%), to settle at $67.6/bbl, while WTI gained $0.9/bbl (+1.4%), to reach $63.6/bbl (fig. 2). According to the Bloomberg consensus of September 19, the price of Brent should fall by $0.9/bbl in the third quarter to settle at $66/bbl, then remain stable at $63/bbl in the fourth quarter (fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 451 Ko)

Read more / Download the dashboard (PDF - 451 Ko)

Â

September 15, 2025

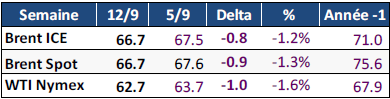

The price of crude is weakening with the prospect of a massive excess supply according to the IEA, but remains supported by a tense geopolitical context and purchases from China. Brent at $67/bbl

Last week, the oil market was caught between two opposing forces: on the one hand, new sanctions against Russia and Iran pose a risk of a drop in supply; on the other hand, the increase in production of the OPEC+ group and the prospect of increasingly large oil stocks weigh on prices (fig. 1 & 2).

At the start of the week, crude oil prices rose by almost 2%, supported by rising geopolitical risks.

The Israeli strike in Qatar, the intrusion of Russian drones into Poland, the Ukrainian attack on Primorsk, Russia’s main oil loading terminal on the Baltic Sea, and the strengthening of American pressure in favor of stricter sanctions against buyers of Russian oil have sharply increased the geopolitical risk premium and revived fears of supply disruptions oil tanker.

This upward trend, however, quickly reversed with the publication of the latest forecasts from the American Energy Information Agency (EIA) and the International Energy Agency (IEA). These organizations have in fact confirmed and amplified the significant excess supply for the coming quarters that they have been announcing for several months, which has caused a significant fall in prices. In this context, hedge funds reduced their bullish positions on oil, particularly on WTI, which reached their lowest level ever recorded.

On a weekly average, Brent for November delivery lost $0.8/bbl (-1.1%) to settle at $66.7/bbl, while WTI lost $1.0/bbl (-1.6%), to $62.7/bbl (Fig. 2). The Bloomberg consensus of September 12 is stable with Brent expected at $67/bbl for the third quarter, and down $1/bbl to $63/bbl in the fourth quarter (Fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 320 Ko)

Read more / Download the dashboard (PDF - 320 Ko)

Â

September 8, 2025

OPEC+ announces a further increase in its production for October. Brent down to $66/bbl

After a relatively stable start to the week, Brent recorded a sharp decline at the end of the week, closing at $65.5/barrel, its lowest level in two months (see figures 1 and 2). Several factors contributed to this decline. On the supply side, while the consensus anticipated that OPEC+ would keep its production levels unchanged at this weekend’s meeting, several statements in the press finally convinced investors that a further increase in production would be adopted, reinforcing expectations of a surplus market. On the demand side, American macroeconomic indicators accentuated the downward pressure: job creation only reached 22,000 in August, while 75,000 were expected. At the same time, oil stocks increased, going against expectations.

Only geopolitical uncertainties continue to partially support prices. Donald Trump urged Europe to stop its purchases of Russian crude, and called for new economic sanctions. Nevertheless, the meeting between Vladimir Putin, Xi Jinping and Narendra Modi at the Tianjin summit last week confirmed that Moscow could still count on its main trading partners, China and India, to sell its oil, thus limiting the potential impact of Western sanctions.

On a weekly average, Brent for October delivery lost $0.7/bbl (-1.0%) to settle at $67.5/bbl, while WTI lost $0.4/bbl (-0.7%), to $63.7/bbl (Fig. 2). The Bloomberg consensus of September 4 is stable with Brent expected at $67/bbl for the third quarter, and $64/bbl in the fourth quarter (Fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 323 Ko)

Read more / Download the dashboard (PDF - 323 Ko)

Â

September 1, 2025

Brent up to $68/bbl with the end of seasonal demand and the rise of OPEC+ supply

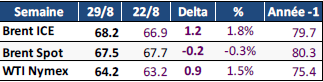

Crude oil prices increased for the second consecutive week, but the general sentiment remains oriented downward (Fig. 1 & 2). The end of the summer driving season in the United States, a traditional period of peak consumption, as well as the OPEC+ meeting scheduled for September 7, during which a new increase in production should be confirmed, are accentuating downward pressure. The macroeconomic context also calls for caution: the increase in customs duties by the Trump administration is reviving fears of a slowdown in global growth and oil demand. In this context, hedge funds have sharply reduced their bullish exposure to American oil, with net long positions falling to their lowest level in almost 18 years, with only 24,225 net long contracts as of August 26, according to the CFTC. Internationally, on the other hand, the trend is the opposite: long positions on Brent have increased, reaching their highest level in three weeks, according to ICE Futures Europe (Fig. 10).Â

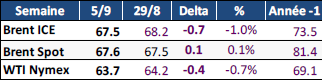

On a weekly average, Brent for October delivery gained $1.2/b (+1.8%) to settle at $68.2/b, while WTI increased by $0.9/b (-0.1%), to $64.2/b (Fig. 2). The Bloomberg consensus of August 29 is stable with Brent expected at $67/bbl for the third quarter, and $64/bbl in the fourth quarter (Fig. 3).Â

Since the start of the year, Brent has fallen by more than 15% to reach $70.2/bbl, compared to the 2024 average over the same period. In euros, the drop is even more marked, with a drop of 17%, due to the fall in the dollar. This drop in the price of crude oil is reflected in the price of fuel at the pump, which fell by an average of 6% for gasoline and diesel over the first 8 months of the year in Europe (Fig. 11).

![]() Â Read more / Download the dashboard (PDF -Â 312 Ko)

Read more / Download the dashboard (PDF - 312 Ko)

Â

25 août 2025

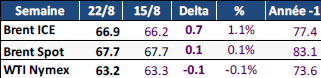

Brent up to $69/bbl between hopes of monetary support and geopolitical tensions

After two weeks of decline, Brent prices resumed their progression last week, approaching $68/bbl, their highest level in two weeks. This progression remains limited, but it marks a slight change in trend. It is partly explained by the sharp drop in American crude stocks, which fell by 6 million barrels last week, much more than expected by the market. At the same time, investors anticipated the decision of the American Federal Reserve, whose president, Jerome Powell, raised the possibility of a rate cut from September during the Jackson Hole conference last Friday. Such a move could boost economic activity and, therefore, support oil demand.

The oil market was also marked by the lack of progress in the conflict between Russia and Ukraine, while

some hoped for the beginnings of appeasement after the discussions held in Alaska and the United States. In response to Russian offensives on its territory, Ukraine has intensified its drone strikes against oil infrastructure in Russia. This strategy led to a sharp rise in gasoline prices in Russia and temporarily disrupted oil deliveries to Hungary via the Druzhba pipeline.

On a weekly average, Brent for delivery in October gained $0.7/b (+1.1%) to settle at $66.9/b, while WTI fell slightly by $0.1/b (-0.1%), to $63.2/b (Fig. 2). According to the Bloomberg consensus of August 22, forecasts remain bullish for the third quarter, with Brent expected at $67/bbl, but are moving downward in the fourth quarter, around $64/bbl (Fig. 3).

![]() Â Read more / Download the dashboard (PDF -Â 379 Ko)

Read more / Download the dashboard (PDF - 379 Ko)

Â

July 21, 2025

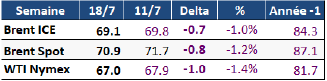

Brent fell slightly to $69/bbl without any precise direction. Tensions on the diesel market are intensifying after new European sanctions against Russia.

In recent days, oil prices have remained generally stable, without any precise direction. The market is awaiting possible major changes regarding sanctions against Russia and the pricing policy of

United States. The 50-day deadline set by the United States for Russia still seems distant, especially since many observers anticipate a reduced application of this measure by President Trump.

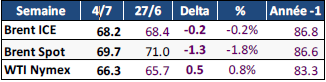

On a weekly average, Brent for September delivery fell $0.7/bbl (-1.0%) to $69.1/bbl, while WTI lost $1.0/bbl (-1.4%) to $67.0/bbl (Fig. 2). The Bloomberg consensus of July 18 is oriented upwards, with a forecast of $67/bbl for Brent in the third quarter (+$1.0/bbl) and $65/bbl for the fourth quarter (Fig. 3).

After a month of June marked by high volatility, oil prices are now stabilizing within a narrow range. Brent is hovering around $70/bbl, supported by high seasonal demand. According to the International Energy Agency (IEA), refining activity is expected to accelerate sharply between May and August, while demand for crude oil for electricity production could reach 0.9 Mb/d during this period. This strength in demand, combined with low inventory levels in some regions, is helping to support prices. However, as fall approaches, the outlook becomes more uncertain. The forward price curve suggests downward pressure as OPEC+ supply increases, while demand gradually slows. Furthermore, uncertainty linked to the application of new sanctions, customs duties and geopolitical tensions, particularly around Russia, continues to weigh on the market. These factors could maintain some volatility, even if prices fall.

![]() Â Read more / Download the dashboard (PDF -Â 883 Ko)

Read more / Download the dashboard (PDF - 883 Ko)

Â

July 15, 2025

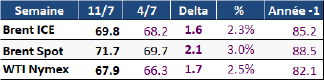

Brent rises to $70/bbl, supported by signals of short-term supply tightening

After a mid-week decline, linked to announcements on new US customs tariffs, oil prices rebounded by more than 2.5% on Friday, supported by signs of short-term supply tightening and by rising geopolitical tensions, particularly in the Red Sea, where Houthi attacks on ships have resumed. Brent finished the week at $70.4/bbl (Fig. 1), while WTI finished at $68.5/bbl, up $1.9/bbl (+2.8%). On a weekly average, Brent for September delivery increased by $1.6/bbl (+2.3%) to reach $69.8/bbl, while WTI gained $1.7/bbl (+2.5%) to reach $67.9/bbl (Fig. 2). The Bloomberg consensus of July 11 is biased downwards, with a forecast of $66/bbl for Brent in the third quarter (down $1.2/bbl) and $65/bbl for the fourth quarter (Fig. 3).