Par Schroders, Global Investor Insight Survey 2026

The conflict in the Middle East (69%) and the uncertainties surrounding American foreign policy and the role of the United States on the international scene (67%) constitute the main geopolitical concerns of investors.

85% of investors are convinced that active management can help them achieve their investment objectives.

Half of investors (50%) now jointly assess the opportunities offered by listed shares and private equity, rather than considering them separately.

Schroders’ annual global investor outlook survey was conducted among more than 1,000 institutional investors, wealth managers and other intermediaries representing $72 trillion in assets.

Faced with geopolitical uncertainties and market concentration, the 2026 edition of the Schroders Global Investor Insight Survey shows that investors around the world are reshuffling their portfolios, thus strengthening their interest in active management.

This survey, conducted among more than 1,000 institutional investors, wealth managers and other intermediaries around the world, collectively representing $72 trillion in assets, reveals that 85% of investors anticipate increased market volatility over the next year. the coming year. They therefore seek to strengthen the resilience and diversification of their portfolios.

Carried out after the outbreak of war in Iran in early 2026, the survey shows that the conflict in the Middle East (69%) and the uncertainties surrounding American foreign policy and the role of the United States in international scene (67%) constitute the main geopolitical concerns of investors. Shocks to commodity and energy prices (53%), a further escalation of geopolitical tensions (52%), as well as an economic slowdown or recession (50%) are also among the events judged most likely to affect their portfolios over the next few years. next twelve months.

Diversification (84%) and protection against market declines and preservation of capital (83%) thus appear to be the main priorities in terms of portfolio management. Furthermore, almost half of investors (47%) say they are strengthening the geographic diversification of their portfolios outside the United States.

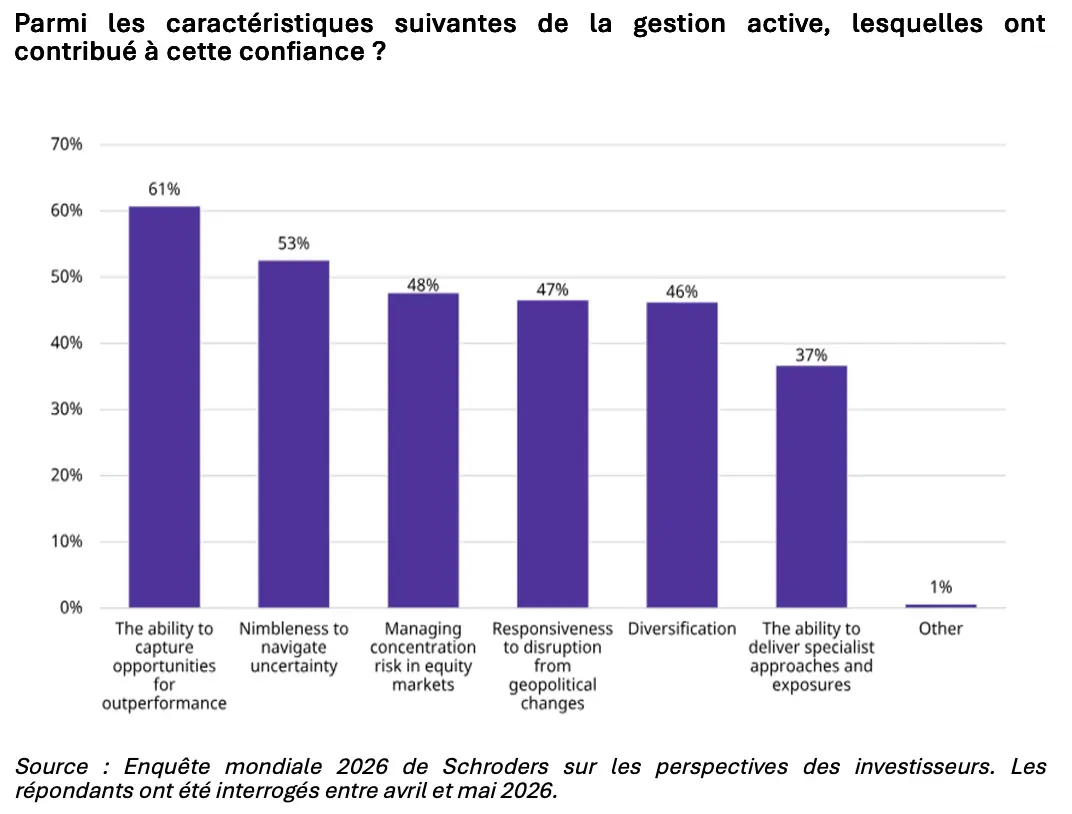

In this increasingly uncertain investment environment, investors show a clear preference for active management: 85% of them believe that it can help them achieve their investment objectives over the next twelve to eighteen months. They consider in particular that it makes it possible to seize opportunities for outperformance, to react with agility in the face of uncertainty and to manage the risk of concentration on the equity markets. A telling sign is that more than a third of investors (38%) are specifically increasing their active management allocations in order to reduce this concentration risk.

For Johanna Kyrklund, Investment Director of the Schroders Group: “In an increasingly volatile world, investors are restructuring their portfolios in order to place diversification and resilience at the heart of their priorities, while taking into account geopolitical risks. It is revealing that, in this context, 85% of investors say they are convinced of the ability of active managers to help them to achieve these objectives over the next twelve to eighteen months.

She adds: “In recent years, we have moved from a globalized world, primarily exposed to deflationary shocks, to a geopolitically fragmented world, in which the reconfiguration of supply chains can fuel inflationary tensions.â€

Active ETFs gain traction as investors seek greater flexibility and efficiency

Active ETFs also occupy a growing place in portfolios. Investors consider them as instruments promoting diversification (49%), tactical positions (42%) and risk management (33%).

For a large majority of investors (70%), the main attraction of active ETFs lies in their costs, which are lower than those of traditional active funds. They also cite daily liquidity and trading flexibility (51%), increased liquidity in the secondary market (43%) and greater portfolio transparency (41%) as their main benefits.

When assessing where an active manager’s expertise can add the most value within an ETF, investors prioritize small and mid-cap stocks (37%), emerging markets stocks (35%), and thematic or sector strategies (34%).

A global approach to listed and unlisted stocks

The survey also shows that investors are taking a more holistic approach to their allocations to listed and unlisted stocks. Half of them (50%) now say they jointly assess the opportunities offered by listed equities and private equity, rather than analyzing them within separate allocation pockets.

Investors are increasingly associating their equity strategies with specific portfolio objectives and no longer consider this asset class as a homogeneous whole. Actively managed fundamental stocks (71%), strategies focused on small and mid-caps (65%), private equity strategies targeting large companies (62%), and private equity in small and mid-sized companies (59%) are considered essential to support long-term growth.

At the same time, stocks focused on dividends or income (74%), long/short or market neutral approaches (33%) and multi-asset strategies (41%) are seen as sources of income. In the area of private equity, 61% of investors particularly highlight the prospects for long-term capital appreciation offered by growth capital and venture capital strategies.

Furthermore, 60% of investors using regional or geographic equity strategies consider macroeconomic and geopolitical uncertainties as a major challenge for their allocation decisions.

All asset classes combined, the five main categories favored to generate risk-adjusted income receive relatively close levels of interest: yield stocks (43%), government bonds used for diversification purposes (38%), listed corporate bonds (35%), high yield bonds (32%) and securitized or asset-backed credit (32%).

These results show that investors are increasingly adopting a holistic, multi-asset approach to generating income, no longer limited to just bonds.

Credit allocations expand in public and private markets

Credit allocations are also evolving. Investors are now seeking a broader combination of cash flow, diversification, resilience and return opportunities, across both listed and unlisted markets.

In listed credit markets, more than half of investors (55%) consider investment grade corporate bonds attractive for generating reliable real income. Furthermore, 62% of respondents see distressed or special situations credit strategies as a source of alpha. High yield bonds and emerging market debt are also seen as sources of alpha by 61% of investors in both cases.

Private credit continues to attract the interest of investors looking for diversified sources of income and potential return. Direct lending is seen as both a reliable source of income (44%) and a potential source of alpha (44%). Investment grade private credit attracts more than a third of investors (36%) in search of stable returns.

Capital resilience is also an important objective of allocations to private credit: 39% of investors cite it as a key driver of their investments in real estate debt, and an identical proportion in infrastructure debt.

Johanna Kyrklund added:“Investors are adapting their portfolios to a more complex and fragmented market. Diversification across regions, asset classes, investment styles and investment vehicles is becoming increasingly important to manage risks and build resilient portfolios. The adoption of a global approach to listed and unlisted assets also transforms the construction of portfolios: investment objectives, considered on the scale of the entire portfolio, now take precedence over traditional references. HAS”

View the full Schroders study

Market analyzes