-

OECD stocks can still absorb a month or two of blockade of the Strait of Hormuz at the current rate of withdrawal; the immediate risk of a supply disruption in developed economies remains limited.

-

Even in the event of a rapid agreement between Washington and Tehran, prices should not fall below 80 dollars per barrel by the end of 2026: reconstitution of stocks and uncertainty over the Iranian nuclear program will support demand.

-

The exit of the United Arab Emirates from OPEC will only have a significant effect from 2027; In the long term, it is the rise in power of the Western Hemisphere that is eroding the cartel’s influence.

Interview with Tom Holland, energy specialist at Gavekal Research

“We are getting to a point where the Western Hemisphere now produces more oil than the Middle East.”

(Tom Holland, Gavekal Research)

Sufficient stocks in the short term, despite the blockade

Simon Pritchard, Gavekal. Tom, over the last few days we’ve heard some pretty apocalyptic warnings that if the United States and Iran fail to reach a deal that would allow the Strait of Hormuz to reopen, we could see a significant spike in oil prices that would take us out of the range we’ve been in for the last two months. What do you think?

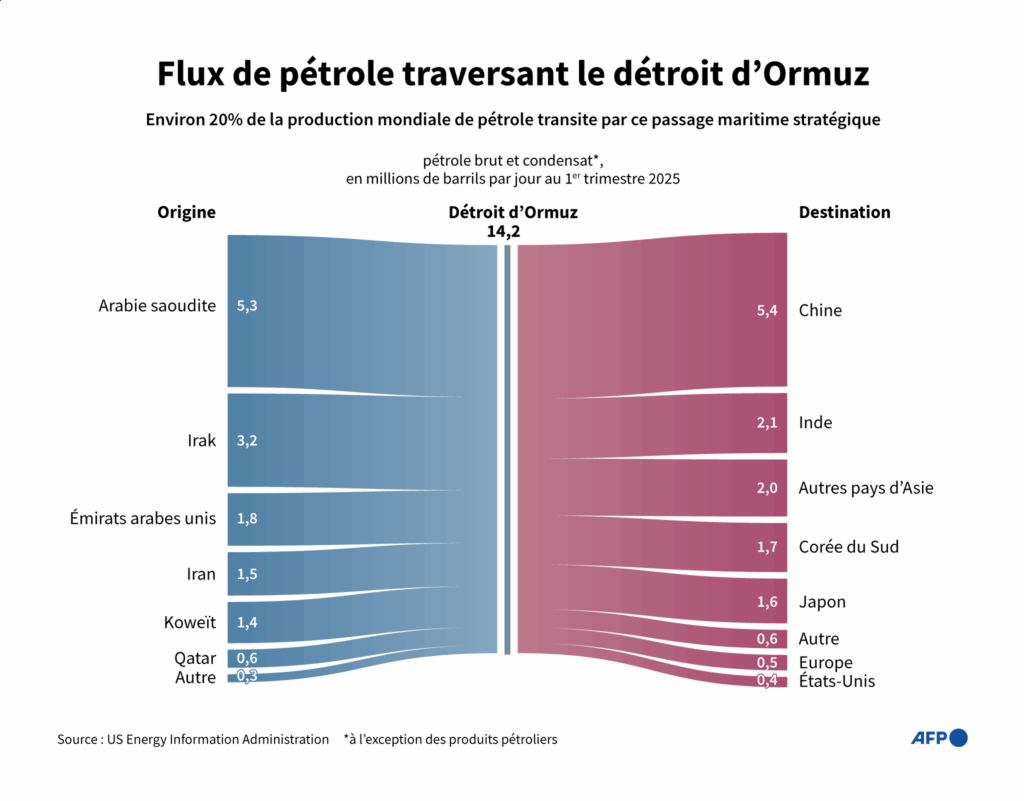

Tom Holland, Gavekal. That’s correct. We have received warnings that the reduction in global oil stocks has continued at such a pace that, if we do not reach an agreement soon, the continued depletion of reserves could restrict supply. According to some oil company executives, prices could rise to 150 or even 160 dollars per barrel within a few weeks. Currently, maritime transport remains largely suspended on both sides of the Strait of Hormuz, and the oil market remains extremely disrupted.

Before this conflict, around 20 million barrels of oil passed through the Strait of Hormuz every day. In recent weeks, this figure has fallen to just a few tankers per day, or perhaps two or four million barrels. Oil trade therefore experienced a massive suspension and the market was supplied by drawing on stocks. Looking across OECD countries, stocks were reduced at a rate of around 5 million barrels per day through April. Obviously this cannot last forever. But the absolute volume of stocks remains quite large: OECD countries have around 2 billion barrels of oil and refined products.

Products (c) AFP

There is of course a catch, in that a large part of these stocks are not really accessible. We cannot simply draw off all the oil that is in the pipelines at a given time, nor that which allows the refineries to operate. It is therefore difficult to know how much additional quantity can be taken. One way to estimate this is to look at how much stocks may have been reduced in the past. It appears that we are not about to run out of oil: stocks can continue to be reduced at this rate for perhaps another month or two.

Beyond commercial stocks, OECD countries also have strategic reserves. The United States Strategic Petroleum Reserve still contains 357 million barrels. Thus, even at a withdrawal rate of one or two million barrels per day, we have sufficient stocks to cope.

“Even at a withdrawal rate of one or two million barrels per day, we have sufficient oil stocks to cope.”

(Tom Holland, Gavekal Research)

This does not mean, however, that there will not be local shortages of specific products. But since crack margins – that is, refiners’ profit margins – have exploded due to this conflict, refiners have a strong incentive to refine as much as possible to provide the necessary products. All things considered, for developed economies, we are not about to experience crippling supply shortages. The consequence is that prices will remain relatively high.

The situation is slightly different in developing countries, and very different in many developing economies where countries might struggle to pay their bills. There is a risk of shortage, particularly in the poorest countries in the world, in Africa for example.

Also read: Iran : problems de péage

What if the strait reopened? Why prices will stay high

Simon Pritchard, Gavekal. So, generally speaking, we expect increased tension if oil traffic through Hormuz does not resume, if Iran and the United States do not reach an agreement in the coming weeks. But what would happen if the strait opened? Should we then expect a collapse in oil prices?

Tom Holland, Gavekal. In the coming days, if an agreement is reached between Washington and Tehran to extend the ceasefire – perhaps for a few months – with the US lifting the blockade of Iranian ports and Iran abandoning its threats against shipping, then we would clearly see a drop in the price of oil. Market participants would sell futures contracts betting on an increase in supply over the coming months.

But prices would not return to the levels of 60 to 70 dollars per barrel which prevailed during the two months preceding this conflict. Several reasons for this. First, a large part of maritime traffic is in the wrong place: supplies will remain limited for a good month after the reopening of the strait. It will also take time for Gulf producers to return production to pre-war levels. Many wells have been closed, and reopening them can be a long, expensive, and even dangerous process. Export facilities, moreover, suffered damage that will need to be repaired. It will therefore take some time before shipments from Gulf countries resume their normal pace.

Beyond that, we noticed a decrease in stocks. Governments and energy companies around the world will seek to replenish these stocks over the coming months. This means high demand for oil. And it’s not just about rebuilding stocks: many countries will seek to build up larger ones. Any short-term agreement between the United States and Iran will in reality only be a preliminary agreement, pending very complex negotiations on the future of Iran’s nuclear program.

If we refer to the JCPOA signed in 2015, these intense negotiations lasted more than eighteen months before the agreement was signed. We also saw negotiations to replace this agreement under the Biden administration: they failed at the last hurdle. These are extremely difficult talks, with very little trust on either side. Thus, for countries around the world – particularly in Asia – which have long depended on energy supplies from the Persian Gulf, it will not only be a question of replenishing their stocks, but of building up larger ones, for fear of a breakdown in negotiations and a return to conflict, or even the suspension of traffic in the strait. of Hormuz.

“The price of oil, according to major benchmarks, is unlikely to fall below $80 per barrel by the end of 2026, even in the event of an interim peace agreement.”

(Tom Holland, Gavekal Research)

So we will have a lot of buyers looking for oil reserves, which will strongly support the price.

Also read: The Strait of Hormuz: illusion of control and geopolitical realities

The withdrawal of the Emirates and the erosion of OPEC

Simon Pritchard, Gavekal. Let’s think about the “supply” side of the equation, after a possible resolution of the blockade. We saw the United Arab Emirates leave the OPEC cartel. There has been much speculation that the pricing power of this cartel is now completely broken. If so, wouldn’t that limit producers’ ability to support prices?

Tom Holland, Gavekal. In the long term, yes. In the medium term, not really. The United Arab Emirates have long felt bitter about the quotas imposed by OPEC. They increased their production capacity and hoped that their quotas would be increased proportionately; they were disappointed by the scale of this increase. They therefore withdrew from the organization and are busy building a second oil pipeline which will allow them to bypass the Strait of Hormuz, connecting the oil fields of Abu Dhabi to Fujairah, on the Gulf of Oman. They will thus be able to go from current production of around 1.5 to 1.7 million barrels per day via this pipeline to a capacity doubled, reaching 3 million barrels per day, or even more. The withdrawal of the United Arab Emirates from OPEC will therefore ultimately lead to an increase in supply. But that won’t happen before 2027.

There is also the question of whether the departure will lead to more rifts within the cartel, with other countries seeking to increase their own quotas or threatening to pull out if they don’t get the increase they want. There is therefore a risk of rupture at this level. But in a broader perspective, OPEC may be becoming less and less important. It regained influence thanks to the agreement with Russia, the OPEC+ cartel.

At present, we do not know what the long-term future of Russian supplies will be, or whether Russia will remain a member of this group. But even so, looking at the global picture as a whole, we are reaching a point where the Western Hemisphere now produces more oil than the Middle East, thanks in large part to growing US supplies. And as much of the oil-importing world has learned the lessons of insecure supplies from potential war zones — whether the Middle East or Russia — producers in the Western Hemisphere, notably the United States, but also Canada and Brazil, are not will stop gaining importance. Which will ultimately further erode the relevance of the OPEC cartel.

In the long term, therefore, yes: the decline of OPEC will lead to a fall in prices. But for now, the market is focused on the short and medium term, and everything indicates that strong demand will continue to support the price of oil.

Also read: Straits and canals: when war threatens the arteries of world trade

Source : Gavekal Research. English translation.